The use of voluntary insurance products has increased significantly, while trust in the insurance sector has reached 60%. These are among the key findings of the nationally representative survey “Public Attitudes and Awareness of Insurance”, conducted by the Trend research agency in May 2026.

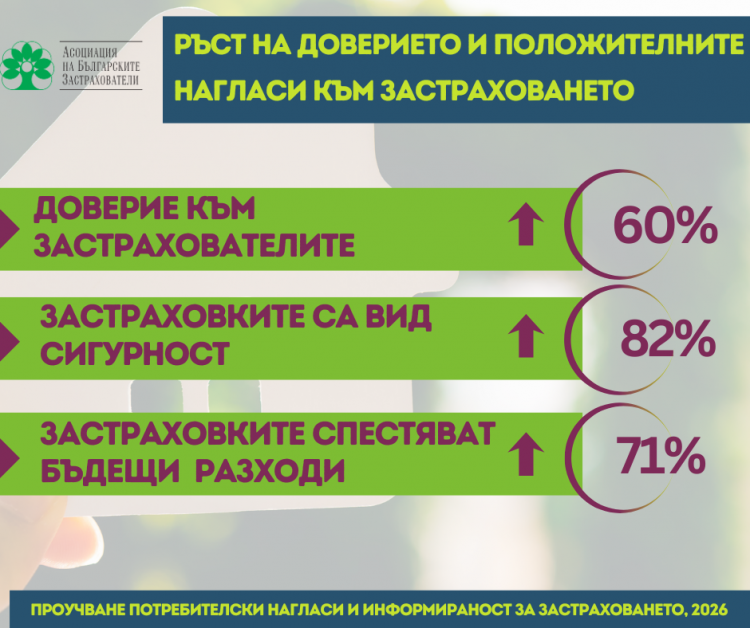

More Bulgarians are placing their trust in insurance companies, while the share of those expressing distrust continues to decline. In 2026, 60% of respondents said they trust the insurance sector, compared with 47% six years earlier, according to the 2020 nationally representative survey on public awareness of and attitudes towards insurance. At the same time, the share of respondents expressing distrust fell from 41% to 31%. The demographic groups with the highest insurance uptake also report the highest levels of trust in the insurance sector. This suggests a direct positive relationship between actual customer experience and trust in insurers.

The findings also indicate a positive shift in the way Bulgarians perceive insurance. The share of respondents who view insurance as a form of financial security has reached 82%, while 71% believe that people should have insurance in order to protect themselves against unexpected future expenses.

At the same time, the use of insurance products has increased across all major voluntary insurance lines. The share of respondents who currently have or have previously had voluntary health insurance has risen from 12% to 27%; borrower insurance from 7% to 17%; and motor own damage insurance (Casco) from 22% to 34%.

The survey also reveals another important development. The share of people who purchase insurance solely because of a legal or contractual obligation has fallen from 59% in 2020 to 32% in 2026. One possible explanation is that insurance is increasingly being perceived not only as an obligation, but also as a voluntary financial protection tool.

The most notable change has been observed in property insurance. The share of respondents who currently have or have previously had property insurance has increased from 16% in 2020 to 31% in 2026.

Attitudes towards protecting property have also changed. The proportion of respondents who believe that the decision whether or not to insure a property should rest with the owner has increased from 51% in 2020 to 65% in 2026.

At the same time, the share of respondents who believe that the state or municipalities should bear responsibility for damaged property has declined from 21% to 14%. Support for compulsory property insurance has also decreased, from 17% to 14%.

These findings may be seen as an indication of a broader shift in the way people perceive the protection of their homes— increasingly viewing it as a matter of personal responsibility and risk management rather than an issue to be addressed by the state or through mandatory regulation.

Thirty-nine per cent of respondents agree with the statement that insurers handle claims fairly. At the same time, an overwhelming majority (83%) of respondents who have actually received an insurance claim payment reported that they were satisfied with it.1 One possible interpretation of these findings is that actual customer experience is more positive than the prevailing public perception of the insurance sector.

The survey also reveals an interesting discrepancy. On the one hand, 82% of respondents describe insurance as a form of financial security, while 71% agree that people should have insurance to protect themselves against unexpected future expenses. On the other hand, only 14% say they would rely primarily on insurance in the event of a serious health- or property-related problem. Respondents are far more likely to rely on their own savings (34%) or on financial support from family and friends (33%).

These findings suggest that although insurance is increasingly recognised as a valuable financial protection tool, it has not yet become the primary mechanism people rely on to manage risk.

Alongside the positive shift in attitudes towards insurance, the survey shows that limited consumer awareness continues to be one of the main challenges facing the development of the insurance market.

Nearly two-thirds of respondents (63%) agree with the statement that people do not understand insurance well enough and therefore do not purchase it, while 57% consider insurance policy terms and conditions difficult to understand. At the same time, only 6% rate their own knowledge of insurance as high, whereas almost half of respondents describe it as limited or non-existent.

This trend is also reflected in the responses of people who do not use insurance products. Among them, 41% say they do not understand insurance well enough, while 44% believe they simply do not need such protection.

The survey also identifies changes in the way consumers search for information about insurance.

An increasing number of people now use digital channels, including insurers' websites, comparison platforms and social media. However, insurance purchases continue to be made primarily through traditional distribution channels. The findings suggest that consumers increasingly research insurance products independently online, while placing growing importance on both the insurer's reputation and professional advice when making their final decision.

The importance of an insurer's reputation as a purchasing criterion has increased from 23% in 2020 to 31% in 2026. At the same time, the share of consumers who consider advice from an insurance adviser to be an important factor has also reached 31%.

The survey findings show that insurance is playing an increasingly important role in Bulgarians' perception of financial security. Alongside growing trust in the sector and higher insurance uptake, there remains a clear need for a better understanding of insurance products and their role in risk management.

Enhancing consumer awareness therefore emerges as a key factor for the further development of the insurance market and for reducing the insurance protection gap. This requires improving consumers' understanding at every stage—from recognising the need for insurance protection and selecting the most appropriate product to understanding policy coverage, terms and conditions, and their rights in the event of an insured loss.

-370x270-3.png "News image")

(002)-370x270-2.jpg "News image")